Transitioning to a more environmentally and socially sustainable world has become an urgent business imperative for banks and other financial services institutions. The financial services sector has a huge role to play in making this transition through the mobilization of capital.

However, sustainability is not only about ethical principles. It also has everything to do with the oldest of banking principles: risk. Climate change and social factors can bring tremendous risk to a bank’s assets and reputation. The environmental, social and governance (ESG) agenda is driven not only by a change in corporate values, but also by customers, regulators, colleagues and investors. This massive, multidimensional challenge can be daunting, but it can also be an opportunity.

Some banks are already well down the ESG path. They have chosen to stop or radically reduce funding of certain sectors. They are actively promoting sustainable financial products. They have baselined their greenhouse gas (GHG) emissions. But most financial institutions are just embarking on the journey, and the sheer scale and depth of the change is top of mind as they wonder: Where should we begin? What should we prioritize?

Our answer? Put in place three essential foundations: an ESG data platform; green IT; an integrated delivery plan. You don’t want to be left behind on this one, in the way that some firms found themselves left behind on digital transformation, the last change of comparable scale in the banking industry.

ESG is not just CSR on steroids

Let’s first take a quick look at ESG’s impact across banking. ESG is not just corporate social responsibility (CSR) on steroids, nor is it a compliance task. It is a massive transformation that requires a fresh mindset and widespread change across the entire organization. Critically, the ESG effort extends downstream in the activities that are financed by the bank and upstream in products and services acquired through the supply chain. Indeed, for most financial services institutions, by far the largest carbon footprint and social and governance impact will be external.

DXC in ESG

With a focus on our customers, people, and communities, we are committed to sustainable and responsible business practices that contribute to a better world.

Learn more

When developing your ESG strategy, you will need to think through what ESG entails across multiple dimensions:

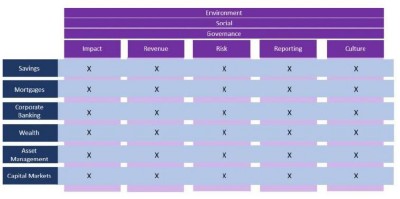

- Impact. Track the ESG impact of loans, investments and other products. Establish new policies for investment that factor in ESG concerns.

- Revenue. Create new products and services that drive brand loyalty, new revenue streams and sustainable outcomes.

- Risk. Assess how climate and social factors may impact all the traditional pillars of financial risk, i.e., credit risk, market risk, liquidity risk. Understand the reputational risk that can come with allegations of greenwashing.

- Reporting. Provide reporting and disclosure for stakeholders, including risk modelling.

- Culture. Embed an ESG mindset in business processes and governance so that this is not an afterthought.

Unlike most transformations that affect just a few parts of the business, ESG plays out across every part of the enterprise, though differently in each area. For example, ESG revenue in capital markets may come from green bonds and social impact bonds; in wealth management from products that allow customers to align investments with their ESG values; and in retail from lower interest rate mortgages for energy-efficient homes, carbon-impact calculators or carbon offset services. When it comes to ESG impact, building societies may want to consider the potential impact on the social mix of a neighborhood if they make loans to gentrify properties, while in corporate banking, loans may need to be linked to the achievement of social or environmental outcomes.

Figure 1 (below) provides a structure for thinking through what ESG means across the bank, so that each of the five ESG dimensions is fully considered by each business unit.

Figure 1. Planning Framework to Integrate ESG in Each Business Unit

In addition to these lines-of-business considerations, ESG will have implications for each support function:

• Risk. Understand risks owing to ESG factors, such as climate events, transition and potential greenwashing.

• Finance. Introduce carbon accounting and carbon budgeting, and track progress towards ESG commitments.

• Compliance and audit. Meet new reporting and disclosure obligations.

• HR. Renew focus on social priorities with more concerted action around diversity, accessibility and inclusion. Leverage the power and higher performance that comes from diverse perspectives and teams.

• IT and Operations. Measure and reduce GHG emissions. Support the business in delivery of ESG initiatives through new data and systems.

• Procurement. Assess vendors’ ESG credentials and the carbon embedded in products and services; count them against the bank’s net zero commitments.

Once ESG is viewed in these terms, the full magnitude of the transition starts to become apparent. No part of the bank will remain untouched.

Data – At the heart of the matter

In our experience, any ESG initiative soon bumps up against constraints around data. Suddenly you need data you weren’t previously collecting, and most of it lies outside the bank. You need sustainability data across the supply chain from Tier 1, Tier 2 and maybe even Tier 3 or 4 suppliers. Downstream you need data on every single counterparty — and for trade finance, for example, even your counterparties’ counterparties.

You also face rapidly evolving reporting and disclosure obligations in nearly every jurisdiction, with often unclear reporting standards and frameworks for the data. In fact, various rating agencies sometimes give conflicting ESG ratings on the same companies.

All of that adds up to a lot of data, much of it new, external, unwieldy, unstructured and subject to interpretation.

To respond to this challenge (and quickly), most banks have simply built ESG into their existing approach to data architecture. The potential risk of this approach, however, is that each business unit defines its own requirements and collects its own data. This works in the short term, but ESG data is just going to grow and grow. Right now, we just see the tip of the iceberg.

In addressing your ESG data needs, you should really take a step back and consider your long-term strategic requirements. Otherwise, you are going to end up building yet another series of data silos, with duplicated data, higher costs and an inability to align decisions around a shared view of data. If you start with the data, you will see that, in fact, many parts of the organization will share a need for very similar data. This includes, for example, data about climate risk, counterparties (customers, suppliers and investments) and aspects of the bank’s own ESG status.

When much of the data is common, the best approach is likely to be an ESG data platform that provides a single source of composable data for business users across the enterprise, eliminating the data siloes that so often undermine bank-wide initiatives. In some cases, the platform can be built by repurposing existing tools. In other cases, a bank might need to build a new platform, perhaps taking advantage of innovations in data management that come through the hyperscalers and other cloud data specialists. In either scenario, a well-managed common data repository ensures that everyone across the bank has secure access to the data that they need when they need it.

For instance, DXC built an ESG data platform to enable a European bank to provide an ESG wealth management solution that lets investors align their portfolios with their personal ESG priorities, whether they favor reducing GHG emissions, preserving biodiversity or creating social impact.

Whatever your chosen technical approach, we can help you establish the foundations of your data platform — designing the architecture, establishing data pipelines, cleaning and structuring the data and making it available for end business users to self-serve — leaving you to focus on making decisions to deliver impact, drive revenue and reduce risk. DXC has also developed relationships with ESG data specialists and has deep partnerships with the hyperscalers and data management firms, so we can help you build out your ESG platform with the right partner ecosystem.

A final change that must be considered is the use of data for decision making. ESG cannot be reduced to a single metric. Different stakeholders value different things. For some, the objective will be to do no harm, perhaps by screening certain sectors; for others, the aim will be to invest in projects that will actively drive sustainable outcomes, such as the preservation of habitats. Still others will prioritize social concerns. The fact that there is a range of objectives calls for much more nuanced decision-making processes, which implies a profound change to governance processes and organizational culture. In order to support these new decision-making processes, decision makers will want a richer set of data, both structured and unstructured, and new analytical tools that can be used to tell a more complex story – say, to evaluate investment in a specific firm or fund.

First steps:

- Identify the data that you will require and how you will source it.

- Establish a data strategy and governance to organize data, accelerate accessibility and enhance usability.

- Enhance your existing data platform or build a greenfield solution, depending on your starting point and your strategy.

- Develop new ESG analytics applications.

- Integrate ESG data into existing models and decision-making and overhaul governance processes, where required.

Green IT: Both part of the problem and the solution

Information technology is both part of the problem and part of the solution. On the one hand, banks are information-intensive businesses and computers are energy hungry. IT accounts for a significant portion of a bank’s direct emissions, so reducing the carbon footprint of IT plays a vital role in meeting net-zero targets. At the same time, IT is crucial for the digitization that is needed to replace physical processes with less carbon-intensive digital processes. For example, the branch of tomorrow is a mobile phone, with a tiny carbon footprint compared to that of a high-street branch network. Training machine learning systems for credit decisioning may be energy intensive, but the alternative — lots of credit officers with laptops in office space — uses more energy.

If you are to square the circle of reducing the carbon footprint of your IT, while using more IT, it becomes imperative to make your technology more energy efficient and move to renewable energy sources.

If you are to square the circle of reducing the carbon footprint of your IT, while using more IT, it becomes imperative to make your technology more energy efficient and move to renewable energy sources.

As a large global IT company, DXC has focused significant effort on improving the environmental side of IT for ourselves and our customers. Since 2019 we have reduced our own direct emissions by 41 percent through a range of interventions, including rationalizing applications, reducing data, moving to a virtual first workplace model (more than 90% of our employees work from home), modernizing data centers and managing the infrastructure more efficiently. We have also committed to set near-term company-wide emission reductions in line with the Science Based Targets initiative (SBTi) and to reduce GHG emissions 55 percent from 2019 levels by 2025.

DXC applies the very same approaches that we have used for our own IT to help customers look at their IT estates — data center, hardware, networking, infrastructure management, applications and data — to create a roadmap for systematically reducing emissions at each level of their IT stack. In fact, we have developed a Transformation Easy Planner tool that assesses an organization’s potential to reduce GHG emissions.

A key component of any roadmap is likely to be doing Cloud Right™, migrating systems to the right hybrid cloud solution and optimizing processing within the cloud to reduce GHG emissions. Because of their massive scale, cloud hyperscalers have major advantages in applying sustainability measures such as server optimization and accessing renewable energy sources. A recent DXC study of How cloud contributes to sustainability goals showed that customers who modernized applications in migrating from on-premises infrastructure to cloud or hybrid IT achieved an average of 37 percent lower carbon emissions.

It’s commonly thought that becoming green necessarily comes with a high price tag. In fact, rationalizing applications, pruning and deleting unstructured data and improving infrastructure management all save money. At the end of the day, we are talking about the most efficient way to store and process data — this reduces costs, as well as carbon. In fact, we have found that moving to the most effective cloud or hybrid IT model reduces total cost of ownership (TCO) by 34 percent.

First steps:

- Set a baseline for current GHG emissions.

- Assess the potential to reduce emissions across your entire IT stack.

- Prioritize GHG reduction interventions and align to your IT roadmap.

- Execute, reset the baseline and repeat.

Delivery: Making it happen through an integrated delivery plan

If you don’t know where to start on your ESG journey, or are wondering what to do next if you already have, you’re not alone.

The key is to get the right balance of top-down and bottom-up action. We’ve frequently seen banks establish a sustainability office at a high level, but the office was not aligned to business units and IT. It is as if, when the sustainability office pulls on a piece of string, nothing happens because it’s not connected to levers of change within the organization. Equally, in too many banks, significant effort is being frittered away by people doing “ESG stuff” in a well-intentioned way, but without any clear priorities as to where the organization can have the greatest impact.

The answer necessarily comes in two parts. First, you need a top-level strategy that defines what ESG means for your customers and other stakeholders. This view of ESG across the five dimensions outlined earlier in this paper (Figure 1) can be cascaded down through the organization to drive priorities and the allocation of resources to deliver ESG outcomes.

Second, change also needs to come bottom-up. In particular, culture change is fundamental so that ESG becomes embedded, rather than an afterthought or lip service. For ESG programs to be successful, people need a genuine understanding of what sustainability means to the organization and how to translate it into real-life action with regards to customers, products and suppliers.

The way to ensure alignment between top-down strategy and bottom-up actions is to create an integrated delivery plan. To help banks gain this alignment and to convert their top-level strategy and goals into action, DXC is partnering with ServiceNow. ServiceNow ESG Solutions allow you to build an ESG strategy that is backed by precise ESG reporting and management. This way you can be sure that projects are in place to deliver your goals and at the same time track their completion, providing all your stakeholders with assurance through ESG disclosure and regulatory reporting.

By way of example, DXC supported a global fast-moving consumer goods company in using ServiceNow to apply ESG metrics to the several thousand global projects that were ongoing so that their impact on ESG could be tracked.

First steps:

- Define goals. Do you actually know what ESG means for your business and your stakeholders? What are your priorities? What actions will have the largest impact on these priorities?

- Secure a tangible board commitment. Is there an ESG budget?

- Cascade goals across the business and be sure that everyone knows how progress will be measured.

- Put measurement systems and processes in place. Track and report progress for new and ongoing projects.

ESG is here to stay, best get started right away

ESG is not a fad. It is not going away. When digital transformation first emerged, some companies realized its significance and took action to digitize their processes. Others did not consider transformation urgent and spent the last decade regretting that oversight. With the scale and depth of the change required for ESG transformation, banks can’t afford to lag behind. There is a relatively long runway, but the size of the change required is massive.

There is nothing to be gained by waiting, and everything to be gained by launching that journey now, with an eye on making your business more sustainable as you also make the world a better place.

About the authors

About the author

David Rimmer is DXC’s lead on Sustainable Finance and ESG in banking and capital markets. David has worked across retail, corporate and investment banking, with clients in Europe, the Americas and APAC.

David is also a research sssociate with DXC Leading Edge. He writes and speaks on emerging technology and its impact on businesses, the economy and society. David has a background in start-ups, having acted as COO of a stock-lending exchange and of an AI company.

Christian Valerius is the director of IT Strategy and Transformation at DXC Technology. Christian leads a team of technology strategy consultants in EMEA that brings client requirements and technology solutions together to create benefits for the banking and capital markets industry. He is part of the ESG team and shapes ESG proposals for individual requirements for central banks or building societies.

Christian has led large transformation projects for a range of industries, including carving out insurance units from banks and implementing a worldwide car financing system with securitization for trading pools of loans on the international refinancing market.